Table of contents

Utilize Flat-Rate Taxation ▶️ Unlock Tax Benefits ✓ Enhance Employee Advantages ✓ Reduce Administrative Overhead ✓ Optimize Your Benefits Here!

MultiBenefits - HERO CARD

With the HERO Card, individual measures become a strong package, tax-free, digital and can be used anywhere.

HR keeps track of things, employees benefit directly.

In today's job market, companies face a central challenge: How do you attract and retain top talent when competition is fiercer than ever? The answer often lies not just in the next pay raise, but in a smarter, tax-optimized form of appreciation. This is precisely where flat-rate taxation comes into play – perhaps your most powerful tool for employee benefits that truly resonate and make a real difference.

This guide is your comprehensive navigator through the jungle of flat-rate taxation. We'll guide you step-by-step through all relevant regulations and show you how to use this tool not just correctly, but strategically. The goal: to boost your team's motivation, reduce ancillary wage costs, and create a company culture where employees feel valued.

Flat-rate taxation is a simplified procedure where the employer assumes the wage tax for certain wage components or non-cash benefits at a fixed percentage and pays it directly to the tax office, instead of calculating it individually based on the employee's tax class.

By the end of this article, you will know exactly which benefits you can tax at a flat rate and how, where the legal pitfalls lie (especially concerning social security), and how to build a benefit system that positions your company as a top employer.

Imagine being able to resolve the complex tax issue for certain salary extras for your entire team with a single, fixed tax rate. That's precisely the principle of flat-rate taxation. Instead of elaborate, individual calculations for each employee, you, as the employer, assume a flat-rate tax. The effect for your employees is enormous: the benefit is received gross for net, without annoying deductions and without additional effort in their own tax return.

To truly understand the advantage, let's take a quick look at the standard approach: individual taxation.

Individual Taxation: This is the classic payroll accounting. Every monetary benefit, such as the private use of a company car, is added to the employee's gross salary. Taxation then occurs according to personal wage tax characteristics, primarily the tax class (I-VI). The result varies for each employee and often involves high deductions for taxes and social security.

Flat-Rate Taxation: Here, a legally defined, fixed tax rate (e.g., 15%, 25%, or 30%) is applied directly to the value of the benefit. You, as the employer, are the sole tax debtor and remit the amount. The tax burden is precisely plannable for you, and individual taxation is completely eliminated for the employee.

With flat-rate taxation, the employer determines the value of a benefit (e.g., a travel allowance) and applies a legally defined flat tax rate to it. The employer remits this tax directly, thereby settling the tax liability for the employee's benefit.

Managing these different rules, tax rates, and exemption limits can seem complex at first glance. However, modern digital benefit platforms completely take this work off your hands. They ensure that every allowance – whether for lunch, commuting, or the gym – is processed automatically and legally compliant. Thus, a tax challenge transforms into an easy-to-use employee motivation tool that strengthens the local economy and excites your team.

Opting for flat-taxed benefits is more than just a nice gesture. It's a strategic decision with tangible advantages for both sides – your company and your employees.

Employers benefit from greatly simplified payroll and reduced bureaucracy. Additionally, flat-rate taxation often allows them to save on social security contributions and enhance their attractiveness as an employer through effective, net-optimized employee benefits.

Abstract theory is best illustrated with a concrete example. Let's assume you want to provide an employee with an additional value of €100.

The result is clear: For lower total costs (€115 instead of approx. €120), your employee receives more than double the net value (€100 instead of approx. €45). This "aha!" moment highlights the enormous efficiency of flat-rate taxation, making it an indispensable tool in modern HR management.

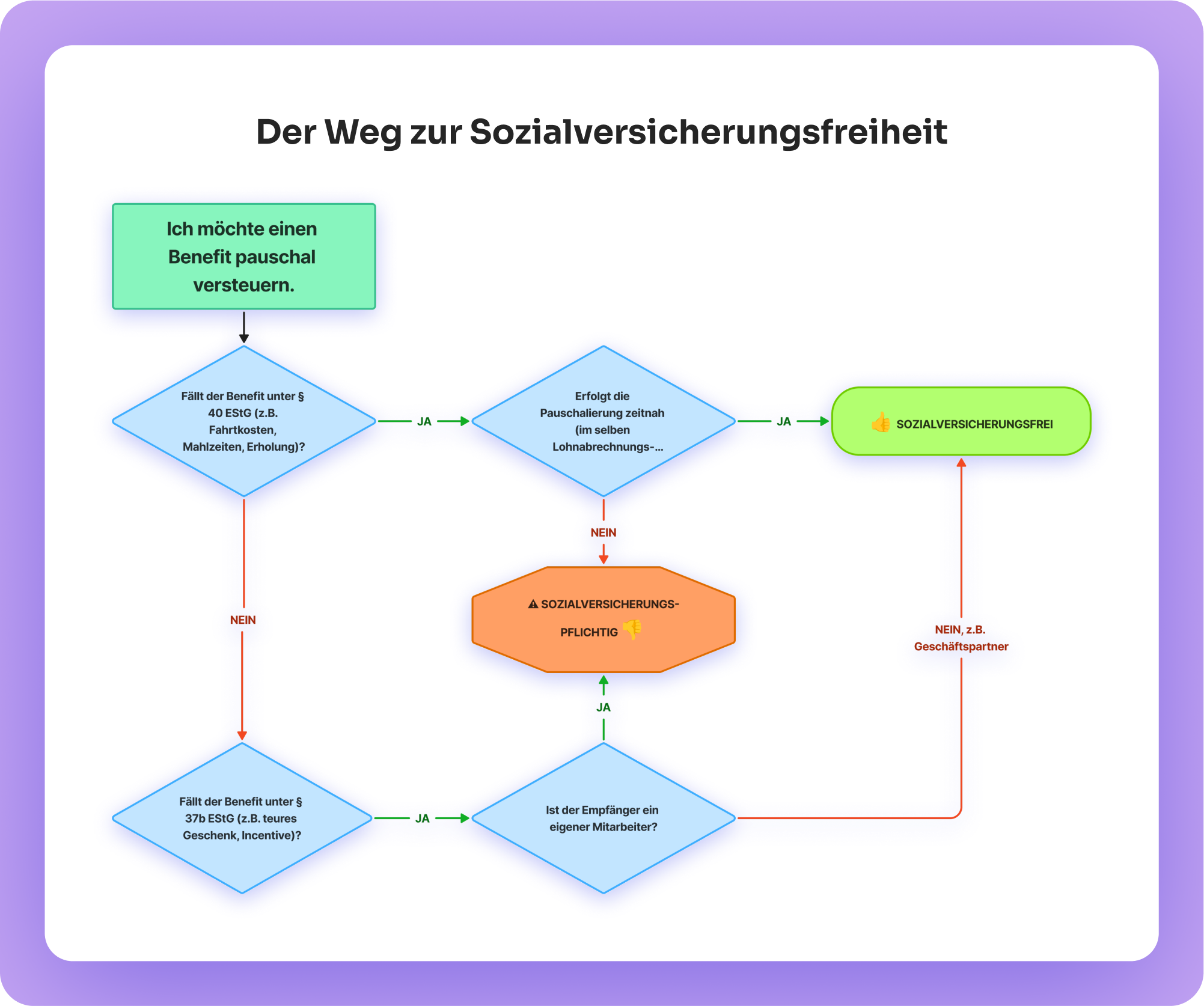

To master flat-rate taxation, you need to understand the two central paragraphs in the Income Tax Act (EStG). They form the foundation of all regulations, but they operate very differently. Their distinctions are crucial for costs, applicability, and especially for the question of social security obligations.

Imagine § 40 EStG as a precise toolkit for the most common employee benefits. This paragraph lists very specific circumstances for which the legislator has provided fixed, usually very advantageous flat-rate tax rates.

Purpose: Targeted tax incentives for socially and socio-politically desirable contributions.

Use Cases: Here you'll find the classic employee benefits, such as:

Tax Rates: The rates are fixed depending on the use case; they usually amount to 15% or 25%.

The crucial advantage: Generally, benefits taxed at a flat rate under § 40 EStG are exempt from social security contributions. This makes them the most cost-efficient option for employee benefits.

If a benefit doesn't fit into the specific framework of § 40 EStG, the general "catch-all provision" of § 37b EStG comes into play. This paragraph allows for flat-rate taxation for a wide range of business-related non-cash benefits and gifts.

Purpose: Primarily an administrative simplification to avoid the recipient (employee or business partner) having to individually declare the benefit for tax purposes.

Application Cases: This regulation applies to benefits that exceed the usual tax-free limits and do not fall under § 40 EStG. Typical examples include:

Tax Rate: The tax rate here is uniform and always 30% (plus solidarity surcharge and church tax, if applicable).

The crucial disadvantage: Non-cash benefits to your own employees, which are subject to flat-rate taxation under § 37b EStG, are generally subject to social security contributions. This makes this form of flat-rate taxation significantly more expensive than the options under § 40 EStG.

The existence of these two separate paragraphs is a deliberate decision by the legislator. § 40 EStG specifically promotes benefits considered socially valuable (mobility, health, recreation) by making them particularly attractive with the bonus of social security exemption. § 37b EStG, on the other hand, serves purely as a simplification rule for other benefits, without this additional financial incentive. For your strategic planning, this means: The hierarchy is clear. First, utilize tax-free limits, then the cost-effective and social security-exempt options under § 40 EStG, and only resort to the more expensive, social security-liable flat-rate taxation under § 37b EStG when necessary.

This table summarizes the critical differences and helps you quickly determine the correct legal classification for a benefit.

Now that we've clarified the legal foundations, let's dive into practice. Which specific benefits can you offer your team and at what tax rate can you apply flat-rate taxation? Here is your catalog of the most popular and effective options.

The Regulation: Subsidies for your employees' daily commutes between home and their primary workplace are a classic. You can apply flat-rate taxation to these at a very advantageous rate of just 15%.

The Requirement: The subsidy you pay must not exceed the amount that the employee could claim as income-related expenses (via the commuter allowance) in their own tax return.

The Advantage: This benefit is exempt from social security contributions for you and your team. For employees with a medium to high income, flat-rate taxation by you is often financially more favorable than deducting the commuter allowance in their own tax return.

Smart Implementation: A modern mobility budget, such as that HERO Ride offers, bundles such subsidies digitally and flexibly. Your employees can use it for public transport, bicycles, or other sustainable forms of mobility. The tax accounting is automated in the background, allowing you to focus on what matters.

The regulation: A daily lunch subsidy is one of the most popular and appreciated benefits. You can apply a 25% flat-rate tax to subsidies for meals consumed on-site or externally.

The requirement: The subsidy must not exceed double the official non-cash benefit value for a meal. For 2025, the non-cash benefit value for lunch or dinner is €4.40.

The advantage: A tangible daily benefit that enhances lunch breaks and boosts team morale. The flat-rate taxation is also exempt from social security contributions.

Smart implementation: Instead of dealing with cumbersome paper meal vouchers, a digital solution like HERO Eats offers your team maximum freedom. They eat wherever they like, simply upload the receipt via the app, and the subsidy is automatically recorded in compliance with tax regulations. This not only strengthens your team but also supports local gastronomy in your region.

The regulation: For company events such as Christmas parties or summer festivals, a tax-free allowance of €110 per employee per event applies. All costs exceeding this amount are considered taxable employment income.

The flat-rate taxation: You can easily apply a 25% flat-rate tax to the excess amount, thereby avoiding individual tax burdens for your employees.

Important note: The flat-rate taxed costs are then exempt from social security contributions. But beware: This only applies if the taxation is carried out promptly! A failure to do so can be expensive, as we will see in the next chapter.

The Rule: You can provide your employees with a financial boost for holidays or other recreational purposes. These recreation allowances can be subject to a 25% flat-rate tax.

The annual maximum limits: The flat-rate allowance is limited to €156 for the employee themselves, €104 for their spouse or civil partner, and €52 for each child.

The Benefit: A wonderful, social security-exempt bonus for holiday savings, which actively supports work-life balance and shows that you care about your team's well-being.

The Scenario: You want to give an employee a high-quality watch worth €500 for their 10th company anniversary. This significantly exceeds both the tax-free limit for gifts on personal occasions (€60) and the monthly €50 non-cash benefit.

The Solution: This is where the general flat-rate taxation rule of § 37b EStG comes into play. You can flat-rate tax the value of the watch (€500) at 30%.

The Cost Calculation: Be careful, this gets more expensive! Your total costs are not just €500 plus €150 flat-rate tax (30%). Since this benefit to an employee is subject to social security contributions, employer and employee social security contributions are also added. The assessment basis for this is the value of the benefit.

The Smart Alternative: For regular appreciation, it is strategically and financially smarter to fully utilize the monthly tax- and social security-exempt €50. With a flexible credit card like the HERO Card (part of HERO Base), employees can save up their credit over months and thus fulfill larger wishes – with full cost control for you and without additional social security burden.

This section is the most important in the entire guide. A mistake here can negate the financial benefits of flat-rate taxation and lead to significant back payments during an audit. The good news: If you know the rules, you're on the safe side.

Not always. Many benefits taxed at a flat rate under § 40 EStG, such as recreation allowances or travel expense reimbursements, are exempt from social security contributions. However, non-cash benefits for own employees taxed at a flat rate under § 37b EStG are generally subject to social security contributions.

Exemption from social security contributions is the biggest financial lever in flat-rate taxation. Securing it must be the top priority. The crucial factor for this is choosing the right paragraph.

We're repeating this because it's so crucial:

This difference can amount to thousands of euros per year for a larger team. Therefore, whenever possible, always choose a benefit that falls under the advantageous regulations of § 40 EStG.

The problem: Imagine you host a fantastic company party in September. When preparing the annual financial statements in March of the following year, your accounting department discovers that the €110 tax-free limit per person was exceeded after all. No problem, you think, and you subsequently declare the 25% flat-rate tax.

The consequence: The tax office will probably accept the retroactive flat-rate taxation of wage tax. However, the German Pension Insurance (DRV) will not, during the next company audit!

The legal basis: The Federal Social Court (BSG) has clarified in a landmark ruling that social security exemption only applies if the flat-rate taxation "is carried out with the wage statement for the respective payroll period" . In plain terms: The flat-rate tax for the September party must also be paid with the September payroll statement (or by October's at the latest).

The risk: Delayed flat-rate taxation leads to full social security contribution liability. This means both employer and employee contributions become due. The financial risk can quickly add up to 40% of the monetary benefit. Thus, a clever benefit turns into a costly oversight.

Theory is good, practice is better. Let's look at how a fictional company, "Muster-Tech GmbH" with 50 employees, strategically modernizes its benefits to succeed in the "War for Talents" – with a limited budget, but maximum impact.

Muster-Tech GmbH's HR department follows a strategic hierarchy for cost-optimized benefits:

First, the foundation is laid: the full utilization of the tax and social security exempt €50 non-cash benefit for all employees.

Implementation: Instead of inflexible fuel vouchers, the company opts for the Regional Hero Card (HERO Base). Each employee receives a monthly credit of €50 on their personal card.

The Advantage: Employees enjoy maximum flexibility and can spend their credit at the local supermarket, their favorite café, or the bookstore around the corner. At the same time, the company actively strengthens the regional economy. For the HR department, administrative effort is minimal, as everything is digital and automated.

Next, a benefit will be introduced that is noticeable every day: a digital meal allowance.

Implementation: Muster-Tech GmbH uses HERO Eats. Employees receive a daily lunch allowance. The process is incredibly simple: Eat out, upload receipt via app, receive allowance. The correct flat-rate taxation of 25% according to § 40 EStG is automatically handled by the system in the background.

The Advantage: A highly valued, social security-exempt benefit that enhances the lunch break and increases employee satisfaction daily.

For the 10th company anniversary, there should be something special.

The Scenario: Each employee receives a high-quality tablet worth €600.

Implementation: Since the tax-free limits are significantly exceeded, the HR department opts for flat-rate taxation according to § 37b EStG.

The Calculation: The HR department calculates the total costs accurately and transparently: €600 (value of the tablet) + €180 (30% flat-rate tax) + the applicable social security contributions on the non-cash benefit. The costs are predictable, but it is consciously accepted that this one-time "wow effect" is significantly more expensive than regularly granted benefits.

Muster-Tech GmbH has put together an extremely attractive package with an intelligent combination of tax-free, social security-exempt flat-rate taxed (§ 40), and strategically utilized, more expensive flat-rate taxed (§ 37b) benefits. It delights employees, is cost-efficient for the company, and positions Muster-Tech GmbH as a modern and caring employer.

Here we answer the most pressing questions that frequently arise in practice.

Generally, it's always the employer. They are the taxpayer liable to the tax office. While theoretically possible to pass the tax burden on to the employee, this is uncommon in practice, as it would negate the positive effect of the benefit.

No. The flat-rate tax has a so-called final withholding effect. This means that the tax matter is fully settled for the employee once the employer has paid the tax. These payments must not and should not appear in the income tax return.

Yes, there are various monetary limits. For general flat-rate taxation according to § 37b EStG, the limit is €10,000 per recipient and fiscal year. Neither the total sum of all benefits nor a single benefit may exceed this amount. For certain flat-rate taxations under § 40 para. 1 EStG (subsequent assessments or other numerous payments), there is a limit of €1,000 per employee per year. Fixed rates (e.g., 25% for recreation allowances) often have their own monetary maximum limits that apply per year.

The €50 non-cash benefit is a monthly exemption limit. Non-cash benefits up to this value are completely tax- and social security-free. Flat-rate taxation, on the other hand, is a procedure for benefits that exceed this limit or do not fall under it, to be taxed at a reduced rate. Both instruments can and should be cleverly combined to maximize the benefit for your team.

Flat-rate taxation is far more than just a mere simplification rule for your payroll. It is a highly effective strategic tool that allows you to effectively increase your team's net salaries, significantly boost employee retention, and position yourself as a modern, caring employer in the competition for top talent.

The key to success is simple and legally compliant implementation. Instead of getting bogged down in legal texts, spreadsheets, and administrative overhead, a digital solution like Regional Hero can automate your entire benefit management. Strengthen your team, lighten the load for your HR department, and simultaneously boost your local economy. Become a hero for your employees.

author

Everything you want to know — simply explained.

Everything you want to know — simply explained.

What is the benefit card?

The HERO Card is a digital Mastercard debit card that allows companies to offer tax-free benefits easily and flexibly. Employees thus receive tax-free subsidies for benefits in kind, mobility, food and health. Everything bundled on one card, individually configurable and implemented in a legally secure manner.

Employees simply pay on a daily basis. Locally in your favorite café or nationwide in supermarkets, pharmacies or public transport.

How does that work for companies?

You control everything centrally in the HR portal.

Activate benefits in five minutes. The HERO Card automatically loads the monthly budget. Digital, secure and tax-compliant.

What are the concrete benefits of this for my team?

Up to 50 euros in kind per month

Meal allowance of up to 7.50 euros per working day

Mobility allowance of up to 58 euros per month

Up to 500 euros per year for health and wellbeing

All tax-free. It's all digital. It's all on one card.

How does HR keep track?

All benefits at a glance. No paperwork.

In the HR portal, you control budgets, see workload and manage everything centrally.

Sign in. Adjust. It's done.

This saves you up to 80 percent of administrative time.

Is that really tax-free?

Yes, all benefits are tax-free for employees and are completely legally compliant. Employers must tax some benefits as a lump sum.

The HERO Card uses legally enshrined allowances. Each category is correctly separated for tax purposes and can be managed automatically.

How much does the HERO Card cost?

As part of the employee license, the card costs 1 euro per employee per month plus charges for charging benefits.

For 50 employees with HERO Base, for example, this equates to around 140 euros per month — less than a joint team meal, but with a long-term effect.

How quickly is the HERO Card ready for use?

Ready to go in just a few days.

Setup, onboarding and go-live take a maximum of one week.

No technical hurdles. Without complexity.